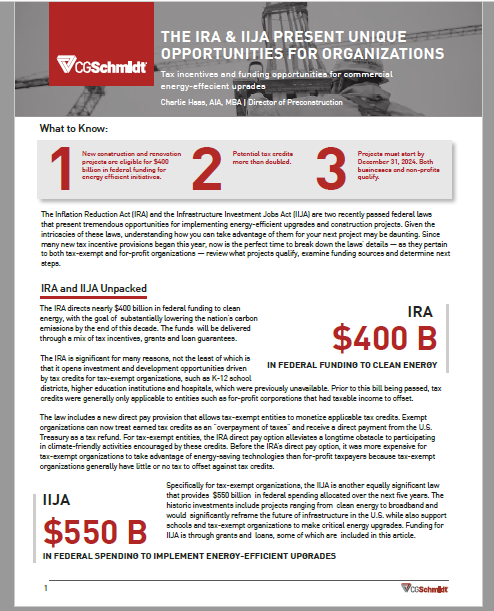

Tax incentives and funding opportunities for commercial energy-efficient upgrades provide pathways for achievement of clean energy goals.

Charlie Haas, AIA, MBA

Director of Preconstruction

CG Schmidt

The Inflation Reduction Act (IRA) and the Infrastructure Investment Jobs Act (IIJA) are two recently passed federal laws that present tremendous opportunities for implementing energy-efficient upgrades and construction projects. Given the intricacies of these laws, understanding how you can take advantage of them for your next construction project may be daunting. Since many new tax incentive provisions began this year, now is the perfect time to break down the laws’ details—as they pertain to both tax-exempt and businesses— review which construction projects qualify, examine funding sources and determine next steps.

IRA and IIJA Snapshot

– New construction and renovation projects are eligible for over $400 billion in federal funding for energy efficient initiatives

– Potential tax credits for construction projects more than doubled

– Construction projects must begin by December 31, 2024 for eligibility

– Both businesses and non-profits qualify

DOWNLOAD THE FULL ARTICLE HERE

IRA and IJJA Unpacked

The IRA directs nearly $400 billion in federal funding to clean energy, with the goal of substantially lowering the nation’s carbon emissions by the end of this decade. The funds will be delivered through a mix of tax incentives, grants and loan guarantees.

The IRA is significant for many reasons, not the least of which is that it opens investment and development opportunities driven by tax credits for tax-exempt organizations, such as K-12 school districts, higher education institutions and hospitals, which were previously unavailable. Prior to this bill being passed, tax credits were generally only applicable to entities such as for-profit corporations that had taxable income to offset.

The IRA’s new approach to tax credit incentives is a game-changer for tax-exempt entities.

The law includes a new direct pay provision that allows tax-exempt entities to monetize applicable tax credits. Exempt organizations can now treat earned tax credits as an “overpayment of taxes” and receive a direct payment from the U.S. Treasury as a tax refund. For tax-exempt entities, the IRA direct pay option alleviates a longtime obstacle to participating in climate-friendly activities encouraged by these credits. Before the IRA’s direct pay option, it was more expensive for tax-exempt organizations to take advantage of energy-saving technologies than for-profit taxpayers because tax-exempt organizations generally have little or no tax to offset against tax credits.

Specifically for tax-exempt organizations, the IJJA is another equally significant law that provides $550 billion in federal spending allocated over the next five years. The historic investments include projects ranging from clean energy to broadband and would significantly reframe the future of infrastructure in the U.S. while also supporting schools and tax-exempt organizations to make critical energy upgrades. Funding for IIJA is through grants and loans, some of which are included in this article.

Qualifying Projects

Both businesses and tax-exempt organizations can now benefit from Section 179D Energy Efficient Commercial Buildings Tax Deduction for energy efficient projects. The deduction itself increased from $1.88 per square foot to up to $5.00 per square foot. For an eligible 250,000 SF building, for example, a $470K deduction at the 2022 rate now potentially increases to a $1.25M deduction. To qualify for the maximum deduction, new construction projects and renovated buildings must meet certain energy-reduction, apprenticeship and prevailing wage requirements. Unlike a tax credit, the deduction reduces taxable income, which results in a smaller decrease in taxes paid, e.g., a business in a 20 percent tax bracket, each $1/SF deduction will be worth $0.20/SF.

While tax-exempt organizations cannot directly utilize the Section 179D deduction, contractors, or other entities responsible for the design of the project can claim it. This then provides an opportunity to negotiate a project cost that is beneficial to both parties. Continuing with the previous example, the $1.25M deduction generates over $400K of tax savings. The tax-exempt organization could agree to allocate the Section 179D deduction to the design and construction team in exchange for a reduction in the overall contract price.

In addition to using Section 179D deductions, companies can use tax credits for upgrades or construction projects. Specifically, Section 148 Investment Tax Credit (ITC) allows building owners to use the tax credit against their own tax liability. In most cases, the credits now carry back three years and forward 20 years. If the owner does not have tax liability or taxable income, then certain credits may be sold to another taxpayer. This concept is known as transferability.

By asking the right questions and working with a trusted partner like CG Schmidt, organizations may be able to take advantage of these government programs and, in turn, reduce the overall cost of energy upgrade projects.

As a company steeped in dedication to green building, CG Schmidt achieved the WELL Health-Safety seal, which recognizes our commitment to advancing human health and wellbeing in our work. We bring WELL methodologies and solutions to our clients for consideration on projects in communities everywhere. By leveraging the expertise of our own WELL accredited professionals, we are uniquely positioned to counsel you on energy upgrade investments and new construction and renovations that meet the IRA and IIJA requirements.

One component of the IRA is driving investment in renewable energy projects that include:

- Wind

- Biomass (closed-loop and open-loop)

- Solar

- Geothermal

- Municipal solid waste

- Hydropower

- Marine and hydrokinetic

- Combined heat and power

- Heat pump

- Energy storage (e.g., batteries)

- Biogas

- Microgrid controllers

Smaller-scale projects to achieve efficiency gains through installations of high-performance components also qualify under Section 179D:

- Interior lighting (not exterior)

- HVAC and hot water systems

- Envelope (roof, windows)

Most of the IRA tax credits are available through 2032,1 but it is important to note that both current and future construction projects may be credit eligible. The date construction begins and the date the property is ultimately placed in service are both critical in determining whether the project is eligible for enhanced credit opportunities. It is necessary to carefully review the type of credit being claimed and the requirements specific to that credit.

If you’re considering a renovation or new construction, both qualify for the 179D deduction. Additions such as a school’s new library or a hospital’s new wing qualify based on the efficiency of only the addition, not the efficiency of the entire/existing structure. The IRA changes to 179D removed the partial deduction related to the separate systems, so the deduction is always based on the efficiency of the project as a whole. Buildings that increase their energy efficiency by at least 25 % will be able to claim this deduction, with bonuses for higher efficiency improvements. The higher level of incentive for large savings is designed to encourage “zero energy ready” projects. In addition, owners can earn 179D benefits every three to four years, as long as a new capital event has led to additional reductions in the building’s carbon footprint.

Funding Opportunities

Buildings-related tax incentives make up for about 14 % of the total clean energy-related resources in the IRA. The IRA provides many tax credit opportunities — even for tax-exempt organizations. In addition to these tax credits and the IRA’s changes to the 179D Energy Efficient Commercial Buildings Tax Deduction, organizations have other sources to help offset the costs of energy upgrades, new construction and renovations. The following includes a few funding opportunities from both the IRA and IIJA summarized for both tax-exempt and for-profit entities.

Applicable to Both For-Profit and Tax-Exempt Organizations:

- Greenhouse Gas Reduction Fund provides grants to support technical and financial assistance to reduce greenhouse gas emissions, functioning essentially as a nation green bank. The U.S. Environmental Protection Agency will administer this $27 billion program, and funding runs February 2023 through September 2024. The fund set asides $15 billion to be targeted to low-income and disadvantaged communities.

Tax-Exempt Organizations:

- Nonprofit Energy Efficiency Materials Pilot Program (IIJA Sec. 40542)

$50M through 2026 for Department of Energy (DOE) pilot program providing nonprofits with grants of up to $200K for building energy improvements, including windows, HVAC, lighting and insulation, for example. Through this pilot program, the DOE will identify scalable models for energy efficiency retrofits in both the nonprofit and other commercial sectors.

- Renew America’s School Grant Program facilitates substantial additional investment that intends to prioritize schools with high needs, minimize administrative burden, and build enduring capacity in local educational agencies and the states to maximize impact equity and efficiency. From keeping schools open to investing in infrastructure, this fund provides financial assistance for a variety of necessary projects to school districts across the country.

- Grants for Energy Efficiency Improvements and Renewable Energy Improvements at Public School Facilities (IIJA Sec. 40541) This competitive grant program can finance the use of clean energy and improvements in energy efficiency and indoor air quality in schools. These enhancements to school buildings can support lower carbon emissions and promote student health. Relevant Eligible Beneficiaries: a consortium of at least one local education agency and at least one school, nonprofit organization, for-profit organization or community partner.

- Eligible improvements covered by these grants include those that result in school energy cost reductions, energy savings and health improvements; involve the installation of renewable energy technologies and electric vehicle infrastructure.

- Priority given to schools serving low-income communities that have the greatest renovation, repair and improvement funding needs, and that can leverage private sector investment through energy-related performance contracting.

- Public School Facilities Grants (IIJA Sec. 40541) Competitive grants to schools and partner organizations (nonprofit and for-profit) over five years (2022-2026) for clean energy improvements at K-12 schools, with priority for schools with renovation/repair needs, lower-income schools and schools using energy-related performance contracting.

For-Profit Organizations:

- Property Assessed Clean Energy (PACE) a financing tool that allows property owners to finance the upfront cost for qualified energy, water, resilience and public benefit projects with funding through a voluntary assessment on the property tax bill. The local government typically acts as the payment collector and remitter. One of the main benefits of PACE for property owners is that it can be used to cover 100 percent of the upfront cost of an energy or resilience upgrade. The investments are then repaid over the useful life of the installed equipment. The longer payback period—and lower annual or semi-annual payments—can make upgrades more affordable for property owners.

- Focus on Energy, in partnership with Wisconsin Public Service, offers energy efficiency rebates and programs to help businesses reduce their energy use and costs. Whether planning a new office building, renovating a school or constructing a multifamily building, Focus on Energy provides opportunities for saving energy. Projects include new construction of commercial, industrial, multifamily and other facilities, buildings undergoing a change of use or adding walls and additions or significant renovations to existing facilities. Installing energy-efficient equipment in new and existing buildings also qualify for financial incentives and rebates.

Timing

To qualify for deductions, construction and energy efficient upgrade projects must begin by December 31, 2024 and be completed by December 31, 2028. However, if the project starts after December 31, 2024 or finishes after December 31, 2028, then it must be carbon neutral.

Invaluable Experience

Application deadlines vary when considering projects that involve grants or loans because of the many government agencies involved. CG Schmidt’s extensive experience in facility planning and budgeting will position your organization to take advantage of these opportunities. Start the planning process, leveraging these tax incentives and federal funding resources as catalysts.

CG Schmidt, a family-owned company since 1920, is a leader in quality construction management, general construction, and design-build services with offices in Madison and Milwaukee. The company serves the markets of education, healthcare, senior living, multi-family, corporate, industrial, community and religious facilities. As a fifth generation, family-owned construction firm, CG Schmidt is a respected industry leader. The company has built a reputation for tackling the most recognizable projects in the state, helping to literally shape the Milwaukee skyline and create quality, state-of-the-art buildings in Madison, the state of Wisconsin and beyond.

Contact us to for more information regarding tax incentives that could financially benefit your next building project.